Either could describe the London office market in Q1. Alexander Peace reports

Has it dodged a bullet or is this just a brief hiatus? Unlike London office investments, which plummeted in Q1, leasing figures held firm.But though some are choosing to seek comfort in numbers which landed ahead of the five-year quarterly average, a growing number of the capital’s agents believe there is bad news to come.

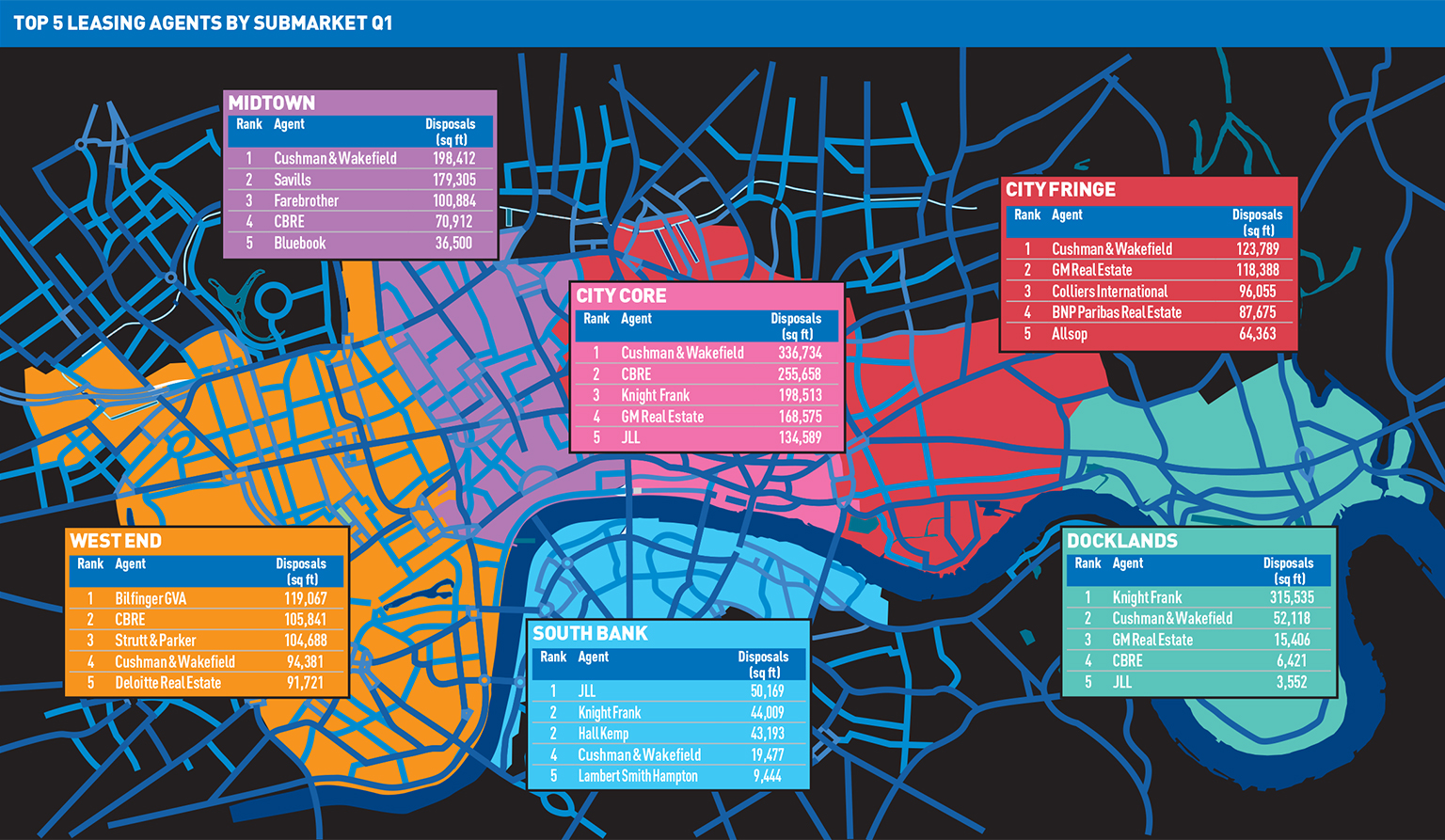

[caption id="attachment_847669" align="alignright" width="400"] Top 5 leasing agents by submarket Q1 2016. Click to enlarge[/caption]

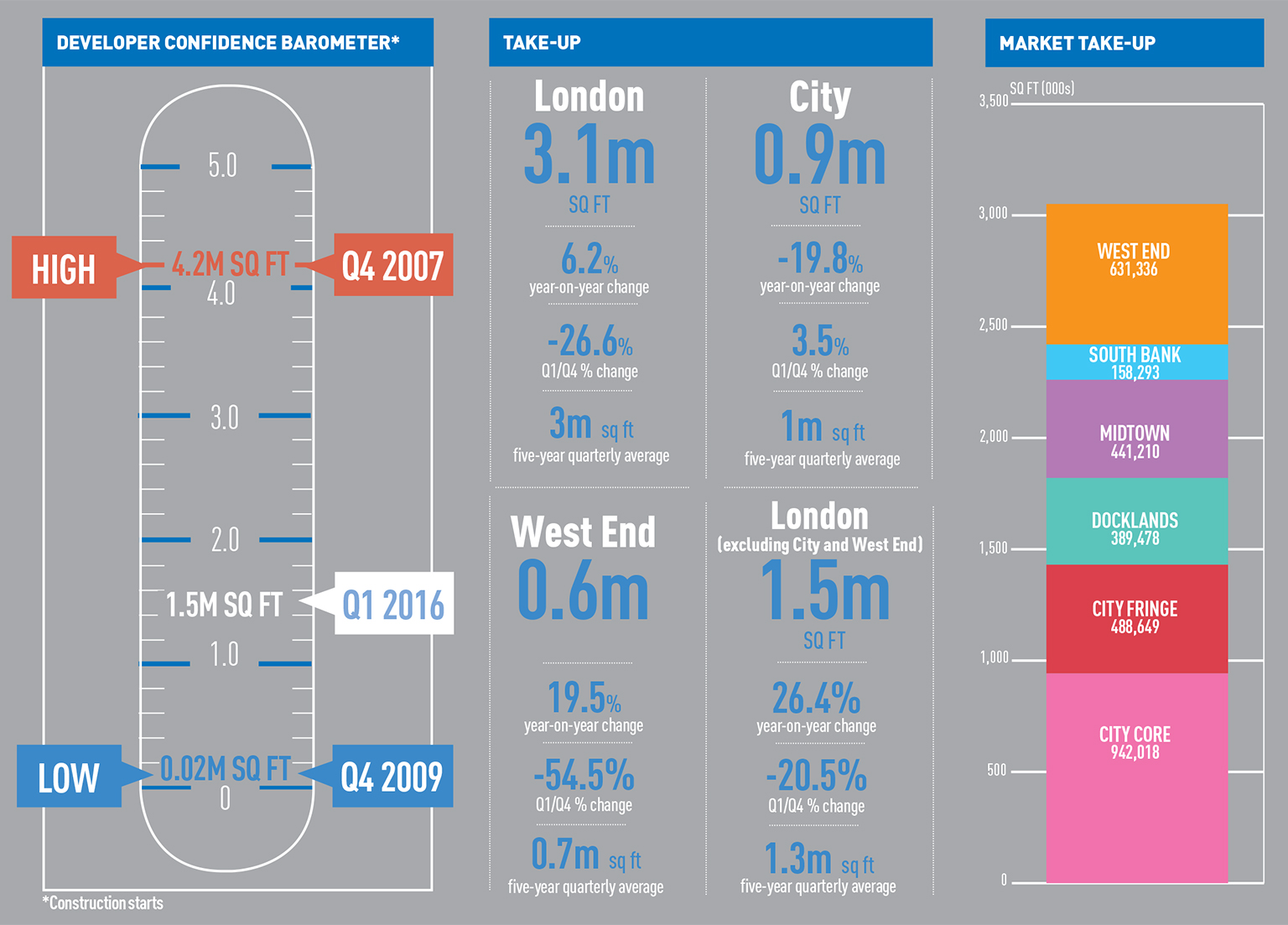

Total take-up across London of 5.1m sq ft was up by 6.2% on Q1 2015, and comfortably above the five-year Q1 average of 2.8m sq ft, according to EGi’s London Offices Research. Thomson Reuters taking 315,500 sq ft at Docklands made 80% of the submarkets total, and seemingly saved the day. Without it, take-up would have slipped by nearly 5% on Q1 2015.

“If I were a betting man, I expect in Q2 the leasing market will catch up with the investment market,” says James Roberts, chief economist at Knight Frank.

“The investment market can very quickly respond to events, whereas the leasing market is shaped by a lot of other considerations.”

And Roberts is not alone. “I would not be surprised if we see the monthly take-up figures dip from now until June,” says Philip Pearce, executive director of central London at Savills. “The sub-5,000 sq ft market is still pretty strong, but north of that there is a pause for breath. Unless you have to trade now, why would you? You would negotiate a deal, but not execute it.”

Average deals sizes took a tumble this quarter, down by a third since Q1 2015. Just 11 deals were signed over the 50,000 sq ft threshold.

And there are other indicators of a weakening market, with availability up for the first time since Q1 2015.

Occupiers still need space though. Much of the demand, according to Adrian Crooks, head of JLL’s West End office, is structural, not expansionary, and – EU referendum or not – he sees it continuing.

Many point back to just 12 months ago and the general election, which failed to have a discernible impact. As Dan Gaunt, head of city agency at Knight Frank, puts it: “These road blocks happen all the way though the city’s leasing market.”

Thomson Reuters and the TMT sector

That said, Knight Frank has cause to be bullish this quarter, acting on 658,000 sq ft of space and moving to second place in the overall agency ranking.

This was aided by its acting on the largest deal of the quarter, that Thomson Reuters sublet of 5 Canada Square, E14, from Credit Suisse. The letting to the media giant was long in the offing, first reported in June last year and finally signed in March.

What it also showed is another strong lease to a TMT occupier which, as a sector, accounted for 32% of take-up this quarter – the largest proportion in the market.

It is certainly not the first time a TMT letting has topped the table, Facebook took 227,000 sq ft at 1 Rathbone Square, W1, last quarter, but it is further proof of the maturity of a sector that was little more than a buzzword four years ago.

Around the markets

The Thomson Reuter’s deal made it a stonking quarter for Docklands, tripling the take-up seen in Q1 2015, and still 50% up on Q4, though such a small market is easy to be influenced by big deals.

A more sedate pace prevailed around the rest of the market, and the mood among agents was as much business as usual as holding back for the referendum.

“You always find Q1 tends to be a bit slower anyway, so the figures are reasonably healthy,” says Elaine Rossall, head of research at Cushman & Wakefield.

In the City, there was a decline in take-up – at 942,000 sq ft, this was 20% down on Q1 2015, though this is still well above the five-year Q1 quarterly average of 809,000 sq ft, and more a result of a busy Q1 last year.

Meanwhile, in the West End, take-up was 21% up on Q1 2015 at 638,000 sq ft, thanks to two big lettings: WeWork taking 107,000 sq ft at 2 Eastbourne Terrace, W2, and Capita committing to 87,000 sq ft at the Copyright Building, W1.

While this shows a degree of confidence in the market, it is important to remember that many of those deals were agreed months ago and, like Thomson Reuters, are only just getting over the line now.

“We were actually pleasantly surprised with the Q1 stats, which were virtually bang on trend,” said Adrian Crooks, head of JLL’s West End office. “A lot of those deals were agreed in Q3 or Q4, but even from a West End perspective, the New Look and Capita deals were sizeable.”

Furthermore, while a TMT letting topped the table, a look at the largest deals of the quarter shows a healthy spread across the occupier types, indicating demand from across the board [see tenant breakdown below].

Alongside those mentioned above, asset manager Investec took 148,000 sq ft in the City at 30 Gresham St, EC2, alongside investment bank Jeffries taking 119,000 sq ft at 100 Bishopsgate, EC3, while New Look took 127,000 sq ft at Kings Cross Central, N1, and AECOM 88,000 sq ft at the Aldgate Tower, E1, in the city fringe.

But while Q1 may have been relatively on form, worry remains around what may happen in Q2.

For many like Chris Valentine, associate director in the JLL West End team, the slowdown represents a hiatus rather than a juddering halt. “From my perspective, there will be a pause for breath prior to Brexit, but I think fundamentally, our market has been underpinned by very robust economics in terms of supply and demand,” he says.

“The worst thing in our market is uncertainty – uncertainty drives inactivity.”

Thomson Reuters: the consolidation

[caption id="attachment_847671" align="alignright" width="300"] 5 Canada Square, E14[/caption]

Thomson Reuters eventually signed its Docklands deal this quarter. Under the deal, all of its London operations will be consolidated under one roof, bar a data centre in Canary Wharf, which means moving out of over eight offices as leases expire.

The deal will also see staff decamp from its 240,000 sq ft letting at the iconic 30 South Colonnade, E14, home of the famous ticker, which will itself be included in the shift, or at least a newer version of it.

According to a spokesman: “Consolidating most of our London operations into one location will reduce complexity, increase collaboration between colleagues, and enable us to better serve our customers.

“5 Canada Square is a prime location where we can remain close to our customers while ensuring minimal disruption to our employees.”

It is set to start moving into the new office from 5 Canada Square, E14, towards the end of the year. The shift from other offices will be phased as leases expire.

That consolidation has already started, with operations at Aldgate House, EC3, where Thomson Financial had 60,092 sq ft, vacated last year.

The elephant in the room

Mergers and acquisitions were always going to be a big theme this year and one that for London started to come through in 2014. But only now are deals such as Colliers International’s takeover of Hatton Real Estate starting to show through.

One agent found itself well clear at the top of the London office agents league table this quarter: Cushman & Wakefield. After finding tenants for 825,000 sq ft, C&W lifted itself head and shoulders above the competition and grabbed the top spot in three markets.

Acting on deals including the Investec and New Look lettings, it worked itself more than 150,000 sq ft clear at the top with wins in midtown and the city fringe, and wrestling the City crown from CBRE.

But with the acquisition of DTZ finally taking effect, did it effectively buy the title?

“When you put together two significant businesses, the market coverage and visibility you get is pretty significant, and we are only at the early stages of reaping the benefits of that,” says Andrew Tyler, head of West End office agency at Cushman & Wakefield.

Knight Frank was pushed into second place, but was top in the Docklands, boosted by its sole agent instruction on the largest deal for the quarter to Thomson Reuters.

CBRE moved down to third and JLL to fourth place. In fact, a relatively slow showing from CBRE and JLL meant quite a shake-up all round, with Bilfinger GVA taking the West End top spot through its 107,000 sq ft WeWork letting.

Central London investment

The capital market

London’s investment market took a hit in Q1 2016, falling by nearly a third on Q4 2015 totals and a double-digit dive compared with the same period last

year.

Total investment volumes of £3.5bn are down by 10% on Q1 2015, and have declined by 32% on Q4 2015 echoing a similar fall in investment volumes nationwide.

West End totals made up almost half the total, or £1.6bn. Notable deals for the quarter include the sale of the Thomas More Square Estate, E1, which Resolution bought from Land Securities for £300m, and Grosvenor’s sale of Almack House in St James’, SW1, for £225m to Pontegadea, Zara founder Amancio Ortega’s property investment company.

CBRE landed the top spot in EGi’s London investment league table, securing £1.4m. JLL was pushed into second as its investment volumes fell by almost one fifth.

Investment agent league table Q1 2016

Agent

Total (m)

Market share

CBRE

£1,253.8

17%

JLL

£1,244.5

17%

Savills

£1,129.4

15%

Cushman & Wakefield

£868.4

12%

GM Real Estate

£615.1

8%

Colliers International

£518.2

7%

Knight Frank

£364.2

5%

Ashwell Rogers

£300

4%

Michael Elliott

£266.9

4%

BNP Paribas Real Estate

£156

2%

Needless to say, the EU referendum is leading to a wait-and-see mentality among investors, with currency declines being one of a raft of reasons cited for delayed investment.

“Investors appear to be taking a pause in terms of investment activity in the city office market,” says Hoong Wey Woon, KPMG UK’s real estate corporate finance lead.

“They are waiting for the situation around the referendum to be resolved. Until this happens, transaction activity is likely to be subdued compared to the past few quarters.”

But alongside delays, there have also been indications of a slowdown in the market, with the price of prime London property looking increasingly high. According to IPD yields, West End and City assets have surpassed their pre-recession lows.

The collapse of Fubon’s deal to buy Cannon Place, EC4, for £500m was a recent blow to the market, though this happened after the Q1 figures were in.

The Taiwanese insurer’s purchase eventually fell through when it was refused regulatory approval.

Seller Hines said it is now in discussions with an alternative buyer.

Other wider macro-economic factors are taking their toll on investment, from Russia to collapsing oil prices and the slowdown in Chinese and emerging market economies.

The Q1 decline is by no means the largest seen in recent years: in Q1 2014, investment volumes fell as low as £1.5bn.

According to Knight Frank’s chief economist James Roberts, investors are like planes above an airport, circling and waiting to make the decision to come in to land.

“The investment market has seen a very distinct drop-off in volume, well below what we have been used to seeing.

“There are a lot of people interested, but I feel as a result of the Brexit, demand has gone into a holding pattern, with political uncertainty scaring off activity.”

The latest take-up figures, submarket analysis and availability rates in the London offices market

Tweet your reactions to @estatesgazette

Follow @EstatesGazette

Click here to receive your free copy of the London Offices Market Analysis

LOMA Q1 2016

Ticking along… or a ticking time bomb?

Either could describe the London office market in Q1. Alexander Peace reports

Has it dodged a bullet or is this just a brief hiatus? Unlike London office investments, which plummeted in Q1, leasing figures held firm.

But though some are choosing to seek comfort in numbers which landed ahead of the five-year quarterly average, a growing number of the capital’s agents believe there is bad news to come.

[caption id="attachment_847669" align="alignright" width="400"] Top 5 leasing agents by submarket Q1 2016. Click to enlarge[/caption]

Total take-up across London of 5.1m sq ft was up by 6.2% on Q1 2015, and comfortably above the five-year Q1 average of 2.8m sq ft, according to EGi’s London Offices Research. Thomson Reuters taking 315,500 sq ft at Docklands made 80% of the submarkets total, and seemingly saved the day. Without it, take-up would have slipped by nearly 5% on Q1 2015.

“If I were a betting man, I expect in Q2 the leasing market will catch up with the investment market,” says James Roberts, chief economist at Knight Frank.

“The investment market can very quickly respond to events, whereas the leasing market is shaped by a lot of other considerations.”

And Roberts is not alone. “I would not be surprised if we see the monthly take-up figures dip from now until June,” says Philip Pearce, executive director of central London at Savills. “The sub-5,000 sq ft market is still pretty strong, but north of that there is a pause for breath. Unless you have to trade now, why would you? You would negotiate a deal, but not execute it.”

Average deals sizes took a tumble this quarter, down by a third since Q1 2015. Just 11 deals were signed over the 50,000 sq ft threshold.

And there are other indicators of a weakening market, with availability up for the first time since Q1 2015.

Occupiers still need space though. Much of the demand, according to Adrian Crooks, head of JLL’s West End office, is structural, not expansionary, and – EU referendum or not – he sees it continuing.

Many point back to just 12 months ago and the general election, which failed to have a discernible impact. As Dan Gaunt, head of city agency at Knight Frank, puts it: “These road blocks happen all the way though the city’s leasing market.”

Thomson Reuters and the TMT sector

That said, Knight Frank has cause to be bullish this quarter, acting on 658,000 sq ft of space and moving to second place in the overall agency ranking.

This was aided by its acting on the largest deal of the quarter, that Thomson Reuters sublet of 5 Canada Square, E14, from Credit Suisse. The letting to the media giant was long in the offing, first reported in June last year and finally signed in March.

What it also showed is another strong lease to a TMT occupier which, as a sector, accounted for 32% of take-up this quarter – the largest proportion in the market.

It is certainly not the first time a TMT letting has topped the table, Facebook took 227,000 sq ft at 1 Rathbone Square, W1, last quarter, but it is further proof of the maturity of a sector that was little more than a buzzword four years ago.

Around the markets

The Thomson Reuter’s deal made it a stonking quarter for Docklands, tripling the take-up seen in Q1 2015, and still 50% up on Q4, though such a small market is easy to be influenced by big deals.

A more sedate pace prevailed around the rest of the market, and the mood among agents was as much business as usual as holding back for the referendum.

“You always find Q1 tends to be a bit slower anyway, so the figures are reasonably healthy,” says Elaine Rossall, head of research at Cushman & Wakefield.

In the City, there was a decline in take-up – at 942,000 sq ft, this was 20% down on Q1 2015, though this is still well above the five-year Q1 quarterly average of 809,000 sq ft, and more a result of a busy Q1 last year.

Meanwhile, in the West End, take-up was 21% up on Q1 2015 at 638,000 sq ft, thanks to two big lettings: WeWork taking 107,000 sq ft at 2 Eastbourne Terrace, W2, and Capita committing to 87,000 sq ft at the Copyright Building, W1.

While this shows a degree of confidence in the market, it is important to remember that many of those deals were agreed months ago and, like Thomson Reuters, are only just getting over the line now.

“We were actually pleasantly surprised with the Q1 stats, which were virtually bang on trend,” said Adrian Crooks, head of JLL’s West End office. “A lot of those deals were agreed in Q3 or Q4, but even from a West End perspective, the New Look and Capita deals were sizeable.”

Furthermore, while a TMT letting topped the table, a look at the largest deals of the quarter shows a healthy spread across the occupier types, indicating demand from across the board [see tenant breakdown below].

Alongside those mentioned above, asset manager Investec took 148,000 sq ft in the City at 30 Gresham St, EC2, alongside investment bank Jeffries taking 119,000 sq ft at 100 Bishopsgate, EC3, while New Look took 127,000 sq ft at Kings Cross Central, N1, and AECOM 88,000 sq ft at the Aldgate Tower, E1, in the city fringe.

But while Q1 may have been relatively on form, worry remains around what may happen in Q2.

For many like Chris Valentine, associate director in the JLL West End team, the slowdown represents a hiatus rather than a juddering halt. “From my perspective, there will be a pause for breath prior to Brexit, but I think fundamentally, our market has been underpinned by very robust economics in terms of supply and demand,” he says.

“The worst thing in our market is uncertainty – uncertainty drives inactivity.”

Thomson Reuters: the consolidation

[caption id="attachment_847671" align="alignright" width="300"] 5 Canada Square, E14[/caption]

Thomson Reuters eventually signed its Docklands deal this quarter. Under the deal, all of its London operations will be consolidated under one roof, bar a data centre in Canary Wharf, which means moving out of over eight offices as leases expire.

The deal will also see staff decamp from its 240,000 sq ft letting at the iconic 30 South Colonnade, E14, home of the famous ticker, which will itself be included in the shift, or at least a newer version of it.

According to a spokesman: “Consolidating most of our London operations into one location will reduce complexity, increase collaboration between colleagues, and enable us to better serve our customers.

“5 Canada Square is a prime location where we can remain close to our customers while ensuring minimal disruption to our employees.”

It is set to start moving into the new office from 5 Canada Square, E14, towards the end of the year. The shift from other offices will be phased as leases expire.

That consolidation has already started, with operations at Aldgate House, EC3, where Thomson Financial had 60,092 sq ft, vacated last year.

The elephant in the room

Mergers and acquisitions were always going to be a big theme this year and one that for London started to come through in 2014. But only now are deals such as Colliers International’s takeover of Hatton Real Estate starting to show through.

One agent found itself well clear at the top of the London office agents league table this quarter: Cushman & Wakefield. After finding tenants for 825,000 sq ft, C&W lifted itself head and shoulders above the competition and grabbed the top spot in three markets.

Acting on deals including the Investec and New Look lettings, it worked itself more than 150,000 sq ft clear at the top with wins in midtown and the city fringe, and wrestling the City crown from CBRE.

But with the acquisition of DTZ finally taking effect, did it effectively buy the title?

“When you put together two significant businesses, the market coverage and visibility you get is pretty significant, and we are only at the early stages of reaping the benefits of that,” says Andrew Tyler, head of West End office agency at Cushman & Wakefield.

Knight Frank was pushed into second place, but was top in the Docklands, boosted by its sole agent instruction on the largest deal for the quarter to Thomson Reuters.

CBRE moved down to third and JLL to fourth place. In fact, a relatively slow showing from CBRE and JLL meant quite a shake-up all round, with Bilfinger GVA taking the West End top spot through its 107,000 sq ft WeWork letting.

Central London investment

The capital market

London’s investment market took a hit in Q1 2016, falling by nearly a third on Q4 2015 totals and a double-digit dive compared with the same period last

year.

Total investment volumes of £3.5bn are down by 10% on Q1 2015, and have declined by 32% on Q4 2015 echoing a similar fall in investment volumes nationwide.

West End totals made up almost half the total, or £1.6bn. Notable deals for the quarter include the sale of the Thomas More Square Estate, E1, which Resolution bought from Land Securities for £300m, and Grosvenor’s sale of Almack House in St James’, SW1, for £225m to Pontegadea, Zara founder Amancio Ortega’s property investment company.

CBRE landed the top spot in EGi’s London investment league table, securing £1.4m. JLL was pushed into second as its investment volumes fell by almost one fifth.

Investment agent league table Q1 2016

Agent

Total (m)

Market share

CBRE

£1,253.8

17%

JLL

£1,244.5

17%

Savills

£1,129.4

15%

Cushman & Wakefield

£868.4

12%

GM Real Estate

£615.1

8%

Colliers International

£518.2

7%

Knight Frank

£364.2

5%

Ashwell Rogers

£300

4%

Michael Elliott

£266.9

4%

BNP Paribas Real Estate

£156

2%

Needless to say, the EU referendum is leading to a wait-and-see mentality among investors, with currency declines being one of a raft of reasons cited for delayed investment.

“Investors appear to be taking a pause in terms of investment activity in the city office market,” says Hoong Wey Woon, KPMG UK’s real estate corporate finance lead.

“They are waiting for the situation around the referendum to be resolved. Until this happens, transaction activity is likely to be subdued compared to the past few quarters.”

But alongside delays, there have also been indications of a slowdown in the market, with the price of prime London property looking increasingly high. According to IPD yields, West End and City assets have surpassed their pre-recession lows.

The collapse of Fubon’s deal to buy Cannon Place, EC4, for £500m was a recent blow to the market, though this happened after the Q1 figures were in.

The Taiwanese insurer’s purchase eventually fell through when it was refused regulatory approval.

Seller Hines said it is now in discussions with an alternative buyer.

Other wider macro-economic factors are taking their toll on investment, from Russia to collapsing oil prices and the slowdown in Chinese and emerging market economies.

The Q1 decline is by no means the largest seen in recent years: in Q1 2014, investment volumes fell as low as £1.5bn.

According to Knight Frank’s chief economist James Roberts, investors are like planes above an airport, circling and waiting to make the decision to come in to land.

“The investment market has seen a very distinct drop-off in volume, well below what we have been used to seeing.

“There are a lot of people interested, but I feel as a result of the Brexit, demand has gone into a holding pattern, with political uncertainty scaring off activity.”

TOP 25 AGENTS Q1 2016

Agency

Disposed

No of deal

Share

1

Cushman & Wakefield

824,912

33

25%

2

Knight Frank

657,868

21

20%

3

CBRE

468,512

41

14%

4

GM Real Estate

330,621

12

10%

5

JLL

298,569

34

9%

6

Savills

263,119

21

8%

7

BNP Paribas Real Estate

226,906

20

7%

8

Colliers International

199,396

41

6%

9

Strutt & Parker

168,471

19

5%

10

Bilfinger GVA

156,175

9

5%

11

Deloitte Real Estate

129,953

6

4%

12

Hall Kemp

116,684

6

3%

13

Farebrother

115,322

15

3%

14

Bluebook

112,474

6

3%

15

HMC Surveyors Limited

87,150

1

3%

16

Allsop

86,682

11

3%

17

Edward Charles & Partners

56,546

12

2%

18

Anton Page

53,803

14

2%

19

Newton Perkins

51,167

12

2%

20

Frost Meadowcroft

37,741

7

1%

21

HNG Limited

37,547

8

1%

22

Monmouth Dean

35,403

8

1%

23

Stirling Ackroyd Limited

31,573

10

1%

24

Ingleby Trice

30,636

7

1%

25

Hanover Green

29,779

7

1%

Back to top

• City: click here

• West End: click here

• Midtown: click here

• City Fringe: click here

• Docklands: click here

• Southern Fringe: click here

• Dashboard: click here

• From the archives: click here

CITY

Top agents Q1 2016: City

Agency

Disposed

No of deals

Share

1

Cushman & Wakefield

336,734

13

35%

2

CBRE

255,658

15

26%

3

Knight Frank

198,513

7

21%

4

GM Real Estate

168,575

4

17%

5

JLL

134,589

19

14%

6

BNP Paribas Real Estate

91,059

11

9%

7

Strutt & Parker

52,492

8

5%

8

Savills

49,039

8

5%

9

Newton Perkins

47,162

11

5%

10

Bilfinger GVA

32,442

4

3%

Back to top

WEST END

Top agents Q1 2016: West End

Agency

Disposed

No of deals

Share

1

Bilfinger GVA

119,067

3

16%

2

CBRE

105,842

15

14%

3

Strutt & Parker

104,688

8

14%

4

Cushman & Wakefield

94,381

9

13%

5

Deloitte Real Estate

91,721

3

13%

6

HMC Surveyors Limited

87,150

1

12%

7

Bluebook

75,974

4

10%

8

Colliers International

73,013

15

10%

9

Knight Frank

67,599

7

9%

10

JLL

63,681

6

9%

Back to top

MIDTOWN

Top agents Q1 2016: Midtown

Agency

Disposed

No of deals

Share

1

Cushman & Wakefield

198,412

4

44%

2

Savills

179,305

5

40%

3

Farebrother

100,884

11

23%

4

CBRE

70,912

5

16%

5

Bluebook

36,500

2

8%

6

GM Real Estate

28,252

3

6%

7

Colliers International

27,368

7

6%

8

Edward Charles & Partners

24,077

2

5%

9

JLL

20,404

2

5%

10

Monmouth Dean

14,862

1

3%

Back to top

CITY FRINGE

Top agents Q1 2016: City fringe

Agency

Disposed

No of deals

Share

1

Cushman & Wakefield

123,789

4

23%

2

GM Real Estate

118,388

3

22%

3

Colliers International

96,055

18

18%

4

BNP Paribas Real Estate

87,675

1

16%

5

Allsop

64,363

4

12%

6

Hall Kemp

60,974

1

11%

7

Anton Page

49,345

12

9%

8

Stirling Ackroyd

31,573

10

6%

9

Pilcher Hershman

28,482

1

5%

10

JLL

26,174

2

5%

Back to top

DOCKLANDS

Top agents Q1 2016: Docklands

Agency

Disposed

No of deals

Share

1

Knight Frank

315,536

1

81%

2

Cushman & Wakefield

52,118

1

13%

3

GM Real Estate

15,406

2

4%

4

CBRE

6,421

1

2%

5

JLL

3,552

1

1%

6

Cherryman

1,030

1

0%

Back to top

SOUTHERN FRINGE

Top agents Q1 2016: Southern fringe

AGENCY

DISPOSED

NO OF DEALS

SHARE

1

JLL

50,169

4

31%

2

Knight Frank

44,009

2

27%

3

Hall Kemp

43,193

1

27%

4

Cushman & Wakefield

19,477

2

12%

5

Lambert Smith Hampton

9,444

3

6%

6

Hanover Green

7,256

1

4%

7

CBRE

5,887

2

4%

8

Capita Symonds

3,227

1

2%

9

Colliers International

2,960

1

2%

10

Workplace Company (The)

2,588

1

2%

Back to top

DATA DASHBOARD

[caption id="attachment_847296" align="aligncenter" width="569"] Click to enlarge[/caption]

TOP FIVE DEALS

[caption id="attachment_847294" align="aligncenter" width="570"] 100 Bishopsgate, EC3[/caption]

Rank

Occupier and building

Size (sq ft)

Market

1

Thomson Reuters, 5 Canada Square, E14

315,536

Docklands

2

Investec (UK), 30 Gresham St, EC2

147,939

City core

3

New Look,Building R7, King's Cross Central, NW1

127,094

Midtown

4

Jefferies Investment Bank, 100 Bishopsgate, EC3

118,575

City core

5

WeWork, 2 Eastbourne Terrace, W2

106,812

West End

Back to top

FROM THE ARCHIVES

• LONDON OFFICES MARKET ANALYSIS: Q4 2015

Back to top

• To send feedback, e-mail alex.peace@estategzette.com or tweet @egalexpeace or @estatesgazette

Top 5 leasing agents by submarket Q1 2016. Click to enlarge[/caption]

Total take-up across London of 5.1m sq ft was up by 6.2% on Q1 2015, and comfortably above the five-year Q1 average of 2.8m sq ft, according to EGi’s London Offices Research. Thomson Reuters taking 315,500 sq ft at Docklands made 80% of the submarkets total, and seemingly saved the day. Without it, take-up would have slipped by nearly 5% on Q1 2015.

“If I were a betting man, I expect in Q2 the leasing market will catch up with the investment market,” says James Roberts, chief economist at Knight Frank.

“The investment market can very quickly respond to events, whereas the leasing market is shaped by a lot of other considerations.”

And Roberts is not alone. “I would not be surprised if we see the monthly take-up figures dip from now until June,” says Philip Pearce, executive director of central London at Savills. “The sub-5,000 sq ft market is still pretty strong, but north of that there is a pause for breath. Unless you have to trade now, why would you? You would negotiate a deal, but not execute it.”

Average deals sizes took a tumble this quarter, down by a third since Q1 2015. Just 11 deals were signed over the 50,000 sq ft threshold.

And there are other indicators of a weakening market, with availability up for the first time since Q1 2015.

Occupiers still need space though. Much of the demand, according to Adrian Crooks, head of JLL’s West End office, is structural, not expansionary, and – EU referendum or not – he sees it continuing.

Many point back to just 12 months ago and the general election, which failed to have a discernible impact. As Dan Gaunt, head of city agency at Knight Frank, puts it: “These road blocks happen all the way though the city’s leasing market.”

Top 5 leasing agents by submarket Q1 2016. Click to enlarge[/caption]

Total take-up across London of 5.1m sq ft was up by 6.2% on Q1 2015, and comfortably above the five-year Q1 average of 2.8m sq ft, according to EGi’s London Offices Research. Thomson Reuters taking 315,500 sq ft at Docklands made 80% of the submarkets total, and seemingly saved the day. Without it, take-up would have slipped by nearly 5% on Q1 2015.

“If I were a betting man, I expect in Q2 the leasing market will catch up with the investment market,” says James Roberts, chief economist at Knight Frank.

“The investment market can very quickly respond to events, whereas the leasing market is shaped by a lot of other considerations.”

And Roberts is not alone. “I would not be surprised if we see the monthly take-up figures dip from now until June,” says Philip Pearce, executive director of central London at Savills. “The sub-5,000 sq ft market is still pretty strong, but north of that there is a pause for breath. Unless you have to trade now, why would you? You would negotiate a deal, but not execute it.”

Average deals sizes took a tumble this quarter, down by a third since Q1 2015. Just 11 deals were signed over the 50,000 sq ft threshold.

And there are other indicators of a weakening market, with availability up for the first time since Q1 2015.

Occupiers still need space though. Much of the demand, according to Adrian Crooks, head of JLL’s West End office, is structural, not expansionary, and – EU referendum or not – he sees it continuing.

Many point back to just 12 months ago and the general election, which failed to have a discernible impact. As Dan Gaunt, head of city agency at Knight Frank, puts it: “These road blocks happen all the way though the city’s leasing market.”

5 Canada Square, E14[/caption]

Thomson Reuters eventually signed its Docklands deal this quarter. Under the deal, all of its London operations will be consolidated under one roof, bar a data centre in Canary Wharf, which means moving out of over eight offices as leases expire.

The deal will also see staff decamp from its 240,000 sq ft letting at the iconic 30 South Colonnade, E14, home of the famous ticker, which will itself be included in the shift, or at least a newer version of it.

According to a spokesman: “Consolidating most of our London operations into one location will reduce complexity, increase collaboration between colleagues, and enable us to better serve our customers.

“5 Canada Square is a prime location where we can remain close to our customers while ensuring minimal disruption to our employees.”

It is set to start moving into the new office from 5 Canada Square, E14, towards the end of the year. The shift from other offices will be phased as leases expire.

That consolidation has already started, with operations at Aldgate House, EC3, where Thomson Financial had 60,092 sq ft, vacated last year.

5 Canada Square, E14[/caption]

Thomson Reuters eventually signed its Docklands deal this quarter. Under the deal, all of its London operations will be consolidated under one roof, bar a data centre in Canary Wharf, which means moving out of over eight offices as leases expire.

The deal will also see staff decamp from its 240,000 sq ft letting at the iconic 30 South Colonnade, E14, home of the famous ticker, which will itself be included in the shift, or at least a newer version of it.

According to a spokesman: “Consolidating most of our London operations into one location will reduce complexity, increase collaboration between colleagues, and enable us to better serve our customers.

“5 Canada Square is a prime location where we can remain close to our customers while ensuring minimal disruption to our employees.”

It is set to start moving into the new office from 5 Canada Square, E14, towards the end of the year. The shift from other offices will be phased as leases expire.

That consolidation has already started, with operations at Aldgate House, EC3, where Thomson Financial had 60,092 sq ft, vacated last year.

Click to enlarge[/caption]

Click to enlarge[/caption]

100 Bishopsgate, EC3[/caption]

100 Bishopsgate, EC3[/caption]